When you begin working with a fund accounting provider, you want to know what to expect from working with your fund accountant on a day-to-day basis. Fundamentally, fund accounting will maintain the books and records for the investment portfolio, perform capital calls and distributions to investors, and provide reporting to management on the disposition and performance of the fund assets. The nature and frequency of that reporting are important to consider closely upon account setup with your fund accounting provider. Two questions should be addressed in detail.

- What specific reporting deliverables should you expect from fund accounting and at what frequency?

- What decisions can be made upon the setup of the fund accounting process that will make reporting as clear and useful as possible for each of the audiences concerned?

It is important to remember at the outset that there will be more than one audience for the reporting that comes from fund accounting. Those different audiences will have different needs and expectations for the presentation they receive.

The Reporting Package

There are five standard deliverables you will expect to receive from your fund accounting firm at a frequency you will determine when you set up the account.

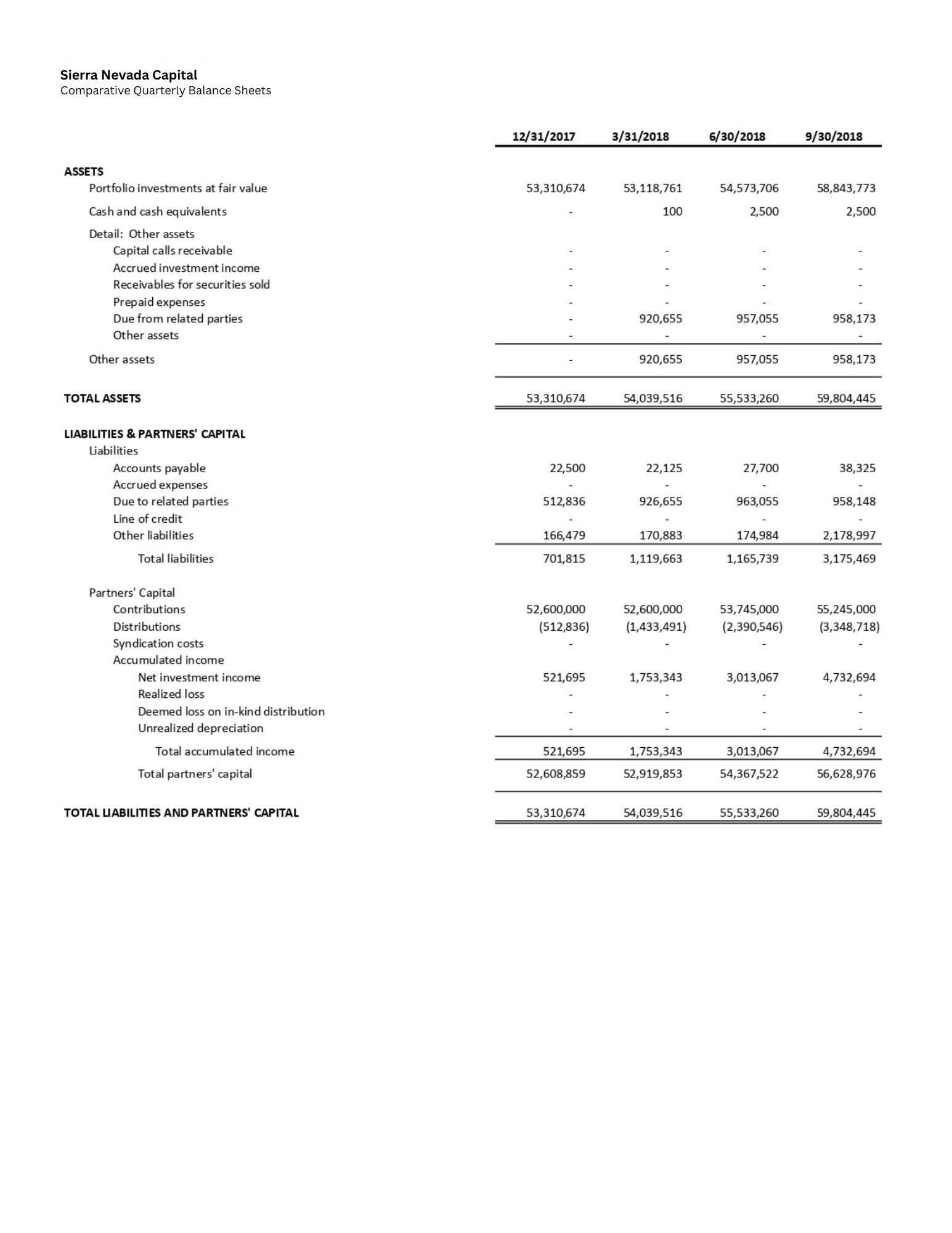

- Balance sheet – This is a snapshot of the assets, liabilities and members’ equity for the fund.

- Income statement – This is a statement of operations: the profits and losses for the stated period. For audit purposes, an income statement is prepared annually. For any other purposes fund accounting can produce it as often as desired. You will decide on the frequency during set up. Quarterly is typical but many funds prefer a more frequent income statement from fund accounting.

- Partners’ capital statement – This is a combination of the balance sheet and income statement. In it, fund accounting shows capital activity contributions, profit and loss activity and what percentage of fund assets belong to the limited partners and to the general partner.

- Statement of cash flows – This is a cash-basis report on three types of financial activities: operating activities, investing activities, and financing activities. Fund accounting will report non-cash activities in footnotes.

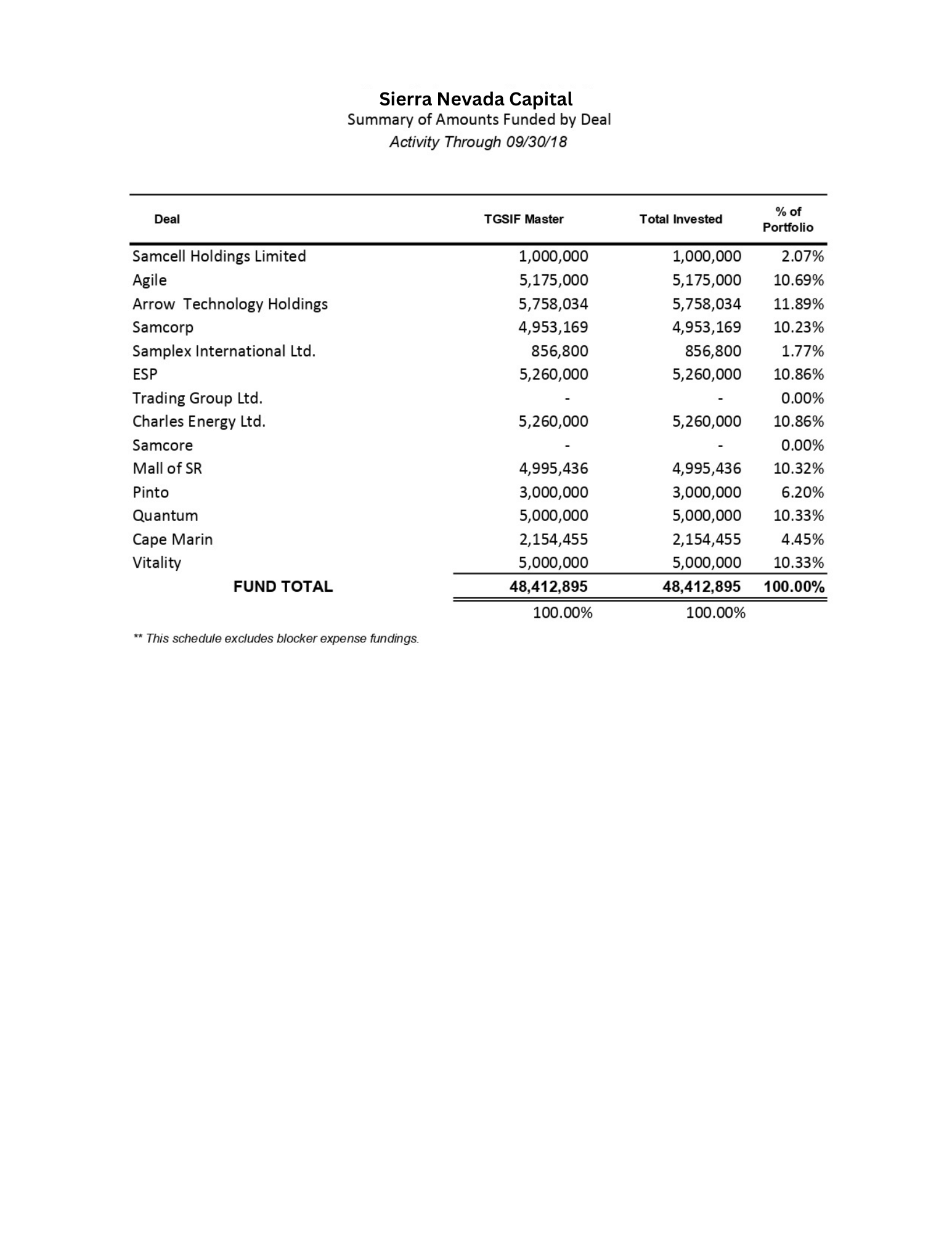

- Schedule of investments (SOI) – this statement provides a complete list of the portfolio assets of the fund, categorized by type of investment, industry, and geography. Fund accounting will separately report investments meeting minimum size thresholds in relation to the fund’s total net value.

Balance Sheet

Partners' Capital Statement

Schedule of Investments

Footnotes to the financial statements are additional information provided by fund accounting which explains how management arrived at the figures on the financial statement. Any irregularities or perceived inconsistencies in fund accounting methodologies are explained in footnotes. Fund accounting provides any relevant disclosures and information on non-cash activities in the footnotes.

This is the standard fund accounting documents package presenting the essential information about the disposition of your fund. For a fund with a master-feeder structure, fund accounting will need to provide some type of consolidated reporting. There is more than one way to have fund accounting approach this. The income statement may have a top section that shows income and expenses at the top level, then a second section showing the same data picked up from the underlying entities. Consolidated statements are only a matter of presentation. The fund accounting document package will include the same five statements reporting the same data, just broken out slightly differently.

Consolidated Statements

The presentation of consolidated financial statements is addressed by Regulation S-X. According to the regulation:

“In deciding upon consolidation policy, the registrant must consider what financial presentation is most meaningful in the circumstances and should follow in the consolidated financial statements principles of inclusion or exclusion which will clearly exhibit the financial position and results of operations of the registrant. There is a presumption that consolidated statements are more meaningful than separate statements and that they are usually necessary for a fair presentation when one entity directly or indirectly has a controlling financial interest in another entity.”

Any attributes that may be relevant to users of this document package should be identified during fund accounting setup so that the appropriate data will be captured and reported.

Multiple Audiences

This is where it is important to remember the multiple audiences for this reporting and to consider what fund accounting can include that will streamline their efforts. For example, if the portfolio includes multiple loans from various countries it will be useful to have fund accounting identify the country for each loan in the schedule of assets or in the footnotes. This may be significant for management and deal teams while less so for auditors and investors. Each of the audiences for fund accounting output will benefit from a presentation and a frequency designed to meet their needs.

- Management – Many managers have fund accounting provide financial reporting quarterly but you can chose any frequency that you prefer including whatever specifics you want to see.

- Auditors – Annual reporting is typical for auditors. Fund accounting should produce audit-quality work papers that are clear, easy to review and cover everything that would be part of a Provided by Client (PBC) list request. This may include calculations and transparency into how the fund accounting system handled the calculations

- Deal Teams – The frequency of fund accounting reporting that deal teams prefer will be in line not only with management reporting but any other deliverables the deal teams may receive relating to the Know Your Client (KYC) process with their partners or tracking leverage and credit facilities. The fund accounting document package may need to be reviewed each time they draw on a credit line. Deal teams will typically be interested in asset-level cash flows and attribution of assets so they can monitor portfolio exposure by geography, deal partners, etc.

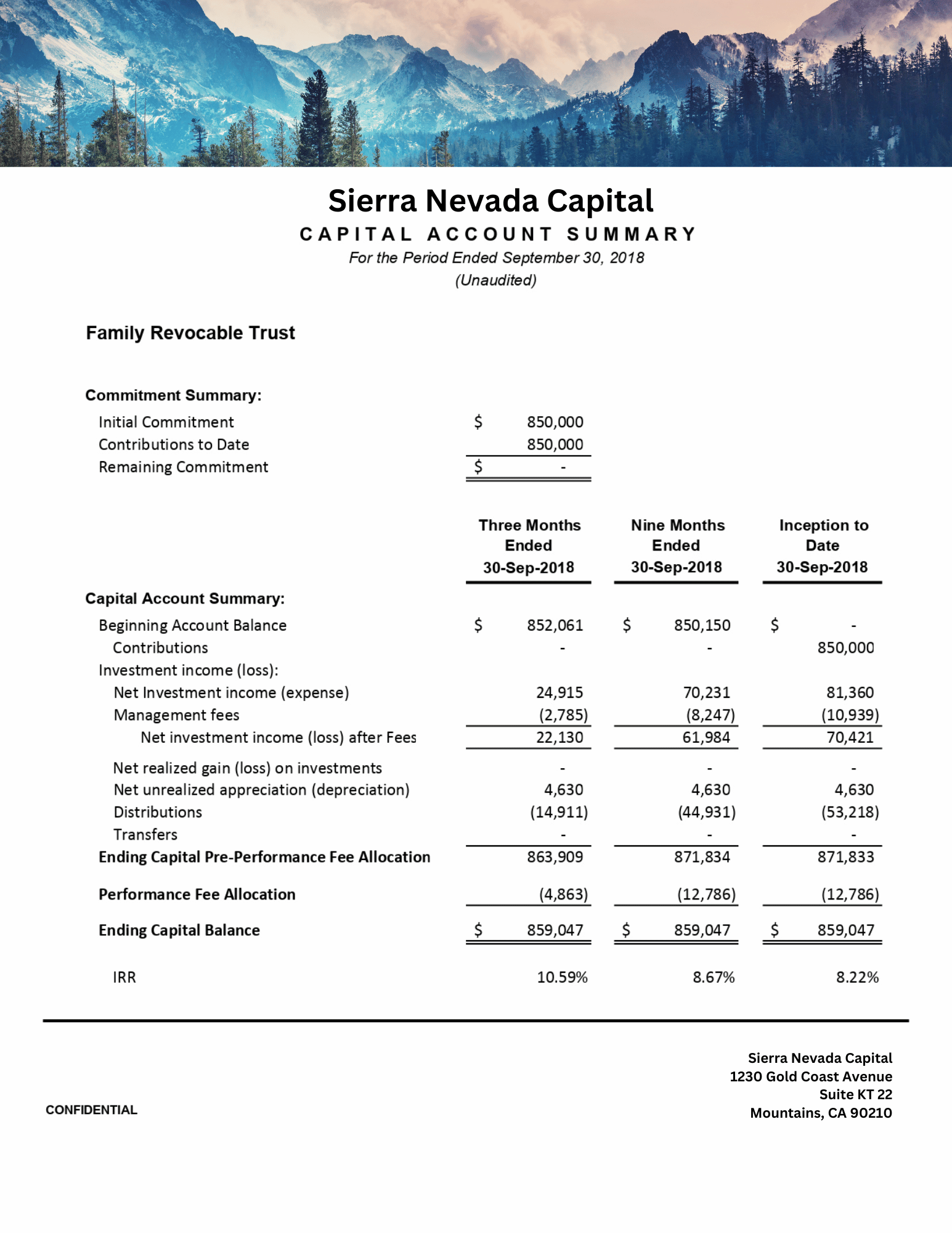

- Investors – Quarterly or monthly statements are most common. The data for fund accounting to include for investor statements depends entirely on what management would like to highlight. Some possibilities are Internal Rates of Return (IRR) by period, a granular breakdown of expenses, or industry metrics such as Distributions to Paid-In Capital (DPI), Total Value to Paid-In Capital (TVPI) or Gross Multiple of Invested Capital (MOIC) so investors can assess the performance of their investment.

Net Asset Value

Periodically, fund accounting will calculate the fund’s Net Asset Value (NAV). In striking the NAV, fund accounting calculates the overall valuation of the portfolio divided by the number of shares to give the per-share value of the security so the investors know the current value of their investment based on the number of shares they own. As private equity funds are long-term investments and often difficult to value, in the past, NAVs were only calculated by fund accounting quarterly or even annually. In recent years, however, as investors demand greater transparency, there is a trend toward bi-weekly or even daily NAVs. There is no longer a standard frequency for NAV calculation. Fund managers will choose to have fund accounting strike an NAV at whatever frequency makes it easiest for them to market their investment product based on investor attitudes. For each calculation of NAV fund accounting will produce of all five of the above documents for management sign-off.