What is Fund Administration?

F und administration is the performance of back-office functions for an investment fund. In terms of the fund’s investment portfolio (the asset side), fund administration involves accounting, tracking and reporting transactions and values for the investment portfolio. In terms of the fund’s shareholders (the investor side), fund administration means maintaining the investor registry and seeing to investor needs and investor-related administrative activity.

Institutional Funds vs. Retail Investor Funds

Among financial services professions, ‘fund administration’ can be a nebulous term. There is no established vocabulary for the third-party fund administration role in the investment fund industry. Managers of institutional funds with only a few pension fund or foundation investors often consider a fund administrator to be simply a fund accountant. Managers of funds with hundreds or thousands of retail investors often engage what they call a fund administrator or a transfer agent to manage the needs of the investors, while separately engaging an accounting firm to manage the fund accounting. Funds with high investor counts have specialized ongoing needs on the investor side:

- Processing of new investments

- Transfers

- Payment of distributions

- Sales commissions

- Investor relations

- Capital calls

- Proxy voting

- Tax document production

- Liaison with financial advisors

- Data dissemination with various industry platforms

These services at scale require systems and processes that many fund administration firms are not able to offer. Some fund administration firms offer services on both the fund accounting and high-volume transfer agent sides, sometimes in addition to other back-office functions including compliance, printing/mailing and web portal solutions.

In-House vs Outsourced Fund Administration

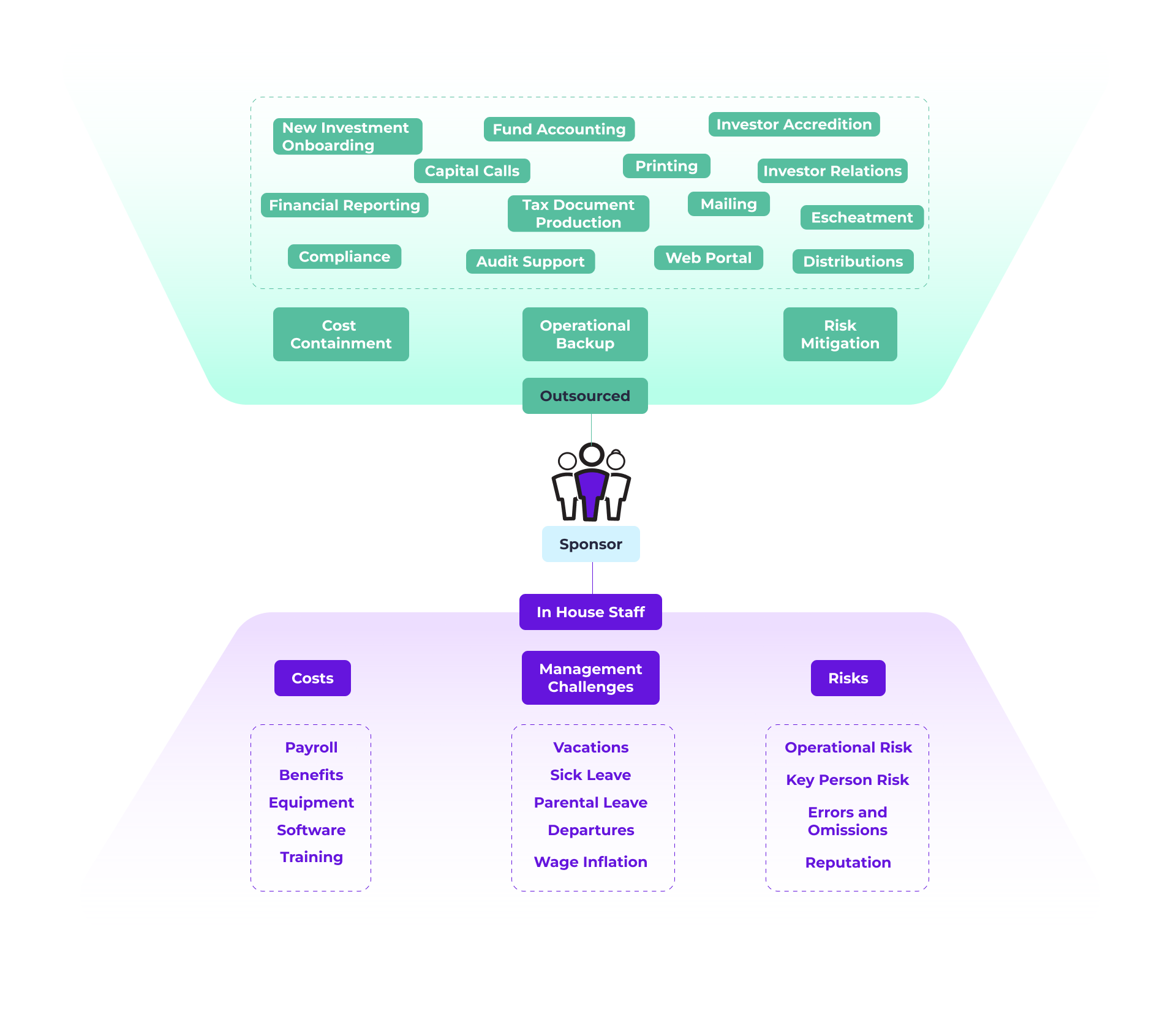

Although publicly-registered funds are required to retain a transfer agent for shareholder management, for many private funds, every aspect of fund administration can be conducted by the fund sponsor using in-house employees. This comes with all the attendant issues of hiring, training, equipping and retaining salaried personnel. There are also potential issues of key man risk involved in an affordable in-house fund administration team.

Many fund sponsors outsource fund administration to accomplish one or more strategic goals:

- To free fund management from the expense and difficulty of employing and managing an in-house fund administration team.

- To be operationally prepared for the scale that comes from success.

- To mitigate the operational risk of key person departures.

- To remove the distraction of non-core back-office functions so that management can concentrate on raising funds and managing assets.

- To isolate the fund administration function as a discrete fund expense.

- To satisfy the concerns of institutions and other large investors who consider in-house fund administration an inherent operational risk.

Outsourced Service Models

Fund administration functions can be outsourced piecemeal or to a single full-service provider. There are many discrete functions within the fund administration role and firms that provide each or several or, in some cases, all of them.

- Fund accounting

- Shareholder management

- New investment processing

- Cash management

- Tax document production

- Compliance

- Investor web portal

- Printing & fulfillment

- Audit support

Outsourcing to multiple of vendors means they will have to communicate and coordinate to accomplish operational tasks. This can cause complications. Full-service fund administration that includes many or all of these functions promotes efficiency, affordability and data security.

Full-service fund administration firms that perform all the back-office functions on both the asset side and investor side and may offer additional services and/or integrated systems capability. Fund sponsors who elect to outsource fund administration should consider the experience, the technology and the service levels of the firms they consider as well as the firm’s ability to support potential future priorities.