SEC Rule 506(c) was introduced on July 10, 2013, as part of the implementation of the Jumpstart Our Business Startups (JOBS) Act, which was signed into law on April 5, 2012. The primary reason for introducing Rule 506(c) was to facilitate easier access to capital for small businesses and startups by allowing them to use general solicitation and advertising when raising funds from accredited investors. This change was aimed at modernizing the securities offering process, making it more efficient for issuers to reach a broader range of potential investors and thereby stimulate economic growth and job creation by easing fundraising constraints for emerging companies.

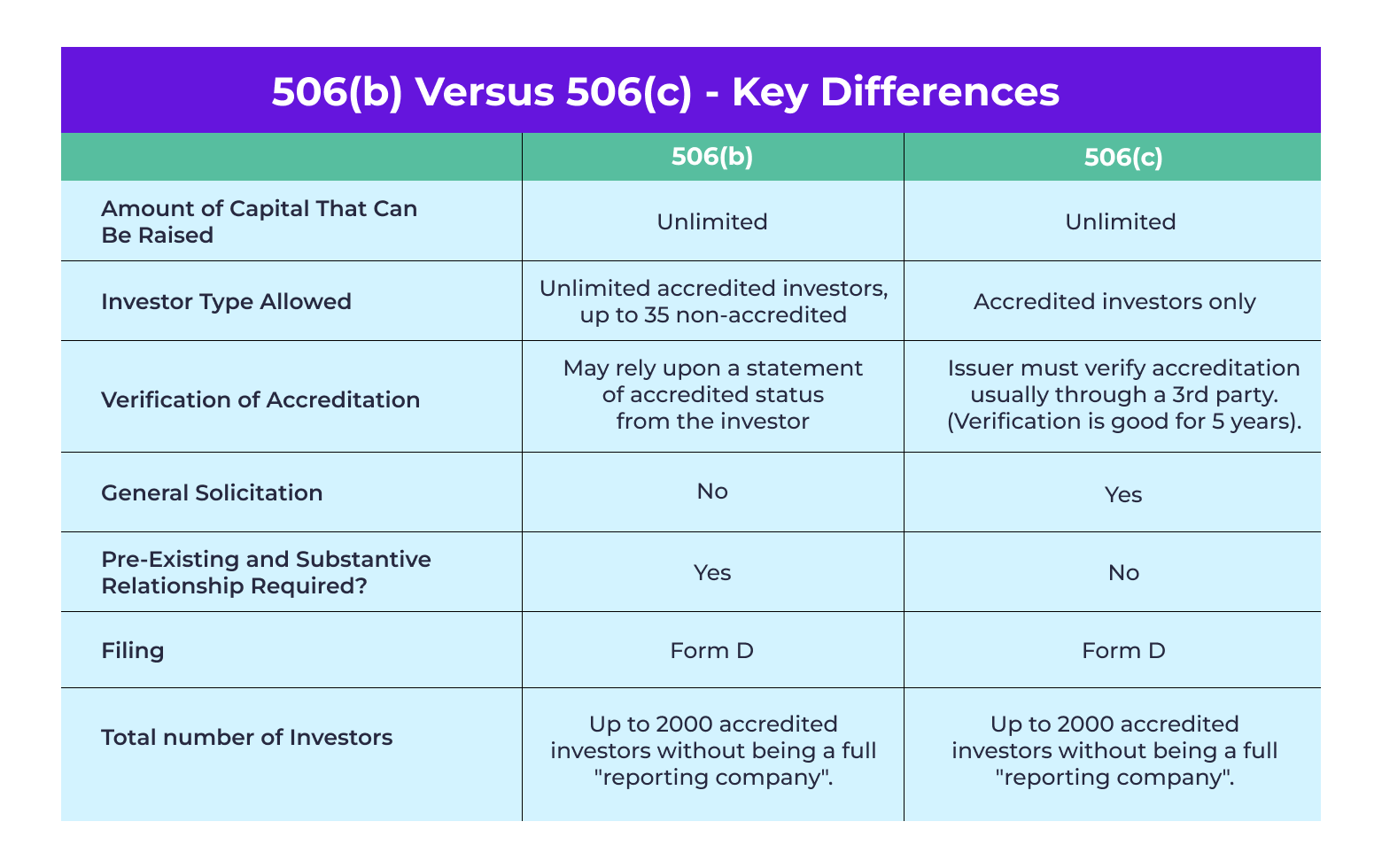

506(c) vs 506 (b)

506(c) differs from Rule 506(b) in that it allows issuers to publicly advertise their securities offerings, but only to accredited investors, requiring issuers to take reasonable steps to verify the accredited status of their investors. Conversely, Rule 506(b) does not permit general solicitation or advertising, but it allows issuers to raise an unlimited amount of money from an unlimited number of accredited investors and up to 35 non-accredited, but sophisticated, investors without needing to verify the accredited status of investors, relying instead on self-certification.

The adoption of Rule 506(c) funds by the investment industry has been gradual. While it offers the advantage of public solicitation, the requirement to verify accredited investor status led some issuers to prefer the traditional 506(b) pathway for its simplicity and the ability to include a limited number of sophisticated, non-accredited investors.

Early Skepticism

Initially, there was significant skepticism around adopting the 506(c) fund structure, primarily due to concerns of disrupting traditional intermediary roles. Market participants feared that allowing issuers to directly approach investors would sideline broker-dealers (BDs) and registered advisors (RIAs), potentially eliminating their roles in the investment process. This apprehension stemmed from the belief that the new structure would not only bypass their services, thus cutting them out of potential earnings, but also diminish the value of their advisory roles to investors.

Despite these initial reservations, the landscape evolved as the industry started to recognize the potential benefits of direct issuer-investor engagement, coupled with mechanisms in place to continue to involve advisors through commission agreements and consultations, addressing the initial concerns. Over time, the ability to broadly market these offerings and the clarity in regulatory compliance have made 506(c) a more and more attractive option. Advisors now appreciate the expanded reach and potential for attracting high-net-worth individuals, and are adapting their strategies to leverage these opportunities.

The Advantages of 506(c)

For an investment fund sponsor, the Rule 506(c) structure offers several distinct advantages. Firstly, it allows for general solicitation and advertising, enabling sponsors to reach a broader audience and potentially attract more accredited investors than would be possible under Rule 506(b). This expanded pool of investors can lead to faster capital raising. Secondly, the requirement to take reasonable steps to verify the accredited status of investors, although initially seen as a burden, can actually enhance the credibility and perceived integrity of the fund, reassuring potential investors of its legitimacy and compliance with regulatory standards. And thirdly, by focusing solely on accredited investors, sponsors can target a wealthier clientele, potentially leading to larger investments and a more financially robust investor base.

The Drawbacks

The Rule 506(c) structure presents some disadvantages as well but less and less over time. Initially, the investor verification requirement could be costly and time-consuming compared to the self-accreditation of 506(b), deterring some sponsors, but accreditation services have emerged and matured from a range of providers over time to allay this concern. Also, while the general solicitation element of the offering can increase the regulatory scrutiny and compliance costs associated with marketing efforts, this only makes the 506(c) option less appealing to smaller funds with limited resources for compliance and marketing.

The Bottom Line

Investment fund sponsors have successfully leveraged the 506(c) structure by embracing its allowance of direct outreach to accredited investors, enabling broader marketing and investment opportunities. This direct approach has facilitated increased capital raising efficiency and transparency, attracting a wider investor base. By integrating digital verification services for accrediting investors and maintaining advisory relationships through strategic commission agreements, sponsors have balanced direct investor engagement with the valuable insights and trust provided by advisors.